Assets (as defined in an earlier blog post) follow a life-cycle – from design and construction, through maintenance and operation, to decommissioning or replacement. During each stage of the life-cycle, an organization must track the right information at the right level to meet legal, regulatory, business, and operational needs. Even if you acquire already built assets, you face the same information challenges and responsibilities, basing your information on asset information you may have acquired.

An organization must meet specific business needs, often varying from department to department, while maintaining a shared set of asset information – a single source of truth to eliminate duplicate data and mitigate version control issues.

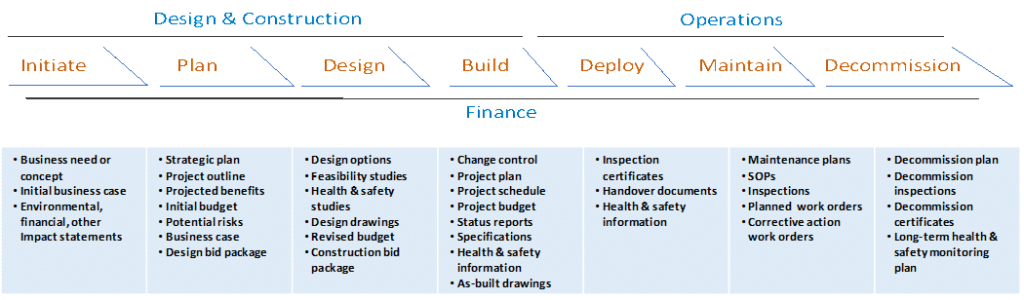

As shown in the figure above, responsibility for assets shifts throughout the asset life-cycle. Typically, Finance manages capital spend, assigning a budget or capital project number. The Design and Construction teams often use this same project number to identify the set of information created during the initial capital project. While this number supports Finance’s immediate need to understand the distribution of its capital budget and supports Construction’s short-term need to manage the construction project, the budget or project number fails as a long-term asset identifier for two reasons.

- Budget numbers are assigned at the project level. Most projects produce more than one asset. The assets must be inspected, maintained, and repaired at a much lower level of granularity than the project budget number allows.

- Given the extensive life of most physical assets – buildings, for example, have an expected useful life of 50 years or more – it is likely that multiple capital projects will impact the same assets over their full life-cycle. An organization must then match project numbers from different fiscal years to the same asset to track the full physical history, including changes and upgrades, for the asset.

At the other end of the spectrum, Operations may identify assets at a very low level of granularity to enable specific maintenance planning, inspections, and repairs. While this level of granularity is helpful to Operations, it is not practical to manage depreciation, taxes, or other organizational reporting requirements at this level of detail.

These disparate business needs are each valid, offering separate but equal views into the organization’s physical assets. However, from an enterprise perspective, these various views present more challenges than solutions when it comes to creating a definitive set of asset information. Asset-centric information management© provides a way to reconcile and manage the asset information across the whole organization and meet these disparate needs – without requiring major business process changes from any one group.